Most Australian borrowers make the same mistake. They spot a low headline interest rate, assume it's the cheapest option, and sign. What they miss is that the headline rate tells only part of the story. Understanding how loan comparison works, and specifically what the comparison rate does and does not include, can save you thousands over the life of a loan. This guide cuts through the confusion so you can compare different loans with confidence, whether you're buying an asset, refinancing, or simply looking for a better deal.

Table of Contents

- Key takeaways

- How loan comparison works in Australia

- The real limits of comparison rates

- Using loan comparison tools effectively

- Home loans vs personal loans: different rules

- Steps to compare loans when refinancing

- My take on what borrowers consistently miss

- Compare smarter with Decentloans

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Comparison rate is standardised | It combines interest plus most fees on a $150,000/25-year benchmark, required by law. |

| It has real limits | Fixed fees weigh heavier on the benchmark than on your actual larger loan amount. |

| Loan type changes the standard | Home loans use comparison rates; personal loans use APR on a different benchmark. |

| Features matter beyond the rate | Offset accounts and redraw facilities affect your true cost but don't appear in comparison rates. |

| Refinancing needs break-even maths | Upfront switching costs must be weighed against ongoing savings before you commit. |

How loan comparison works in Australia

The term "comparison rate" is the formal, legally required figure you'll see displayed alongside every advertised home loan rate in Australia. It's not just marketing. The comparison rate combines the interest rate with most mandatory fees into a single annual percentage, giving you a more complete picture of what a loan actually costs.

Here's what the comparison rate includes:

- Interest rate

- Establishment fees

- Ongoing monthly or annual service fees

- Valuation fees

And here's what it leaves out:

- Government charges (stamp duty, mortgage registration)

- Break costs on fixed loans

- Redraw fees

- Fee waivers or promotional discounts

The benchmark used for every home loan comparison rate is a $150,000 loan over 25 years. That figure is set by law under the National Consumer Credit Protection Act. Every lender must display this figure next to their advertised rate, which is what makes it useful for side-by-side comparisons.

Pro Tip: Always look at both the headline rate and the comparison rate together. A big gap between the two signals high fees, which matters more the smaller your loan is.

The real limits of comparison rates

The comparison rate is a helpful starting point, but relying on it alone is where many borrowers go wrong.

The biggest issue is the benchmark itself. Because the comparison rate is calculated on a $150,000 loan, fixed-dollar fees disproportionately inflate the comparison rate on that small baseline. If you're borrowing $600,000, a $500 establishment fee has far less proportional impact than the comparison rate suggests. In other words, the comparison rate can overstate the real cost of a loan for larger borrowers.

Fixed-rate loans have another quirk. The comparison rate for a fixed loan assumes you'll revert to the lender's standard variable rate once the fixed term ends. That revert rate is often high. In reality, most borrowers refinance or renegotiate before that happens, so the comparison rate may paint a worse picture than your actual experience.

Then there are features the comparison rate simply ignores. Offset accounts reduce effective interest costs meaningfully over time, but that benefit is invisible in the comparison rate calculation. The same goes for redraw facilities, extra repayment flexibility, and fee waivers.

A loan with a slightly higher comparison rate but a fully functional offset account could cost you significantly less over 20 years than a "cheaper" loan with no offset. The number on the page doesn't show you that.

Using loan comparison tools effectively

Knowing what comparison rates mean is half the battle. Using comparison tools well is the other half. Here's a practical order of operations that experienced brokers follow.

-

Define your loan details first. Know your loan amount, preferred term, and purpose before you open any comparison tool. Loan purpose and amount first should always come before detailed cost comparison.

-

Apply filters that match your situation. The best loan comparison tools let borrowers filter by loan-to-value ratio (LVR), fixed versus variable rate, and owner-occupier versus investor purpose. These filters change the rates and fees displayed significantly.

-

Compare the full cost picture. Look at both the headline rate and the comparison rate, then adjust mentally for your actual loan size. A $600,000 borrower should weight fees less heavily than the benchmark implies.

-

Check features against your behaviour. If you'll park savings in an offset account, that feature is worth paying a slightly higher rate for. If you won't, don't pay for it.

-

Calculate total repayment cost. Most comparison tools include a repayment calculator. Use it. Total cost over the loan life is the most honest number you can look at.

| What to compare | Why it matters |

|---|---|

| Headline interest rate | Drives the bulk of your repayments |

| Comparison rate | Signals fee load relative to the benchmark |

| Total repayment cost | Most accurate measure for your actual loan |

| Offset/redraw features | Can reduce effective interest significantly |

| Break and discharge fees | Critical if you plan to refinance early |

Home loans vs personal loans: different rules

This is where borrowers frequently get confused. Home loans and personal loans do not use the same comparison standard, so you cannot directly compare figures across the two.

The home loan comparison rate is based on a $150,000 loan over 25 years. Personal loan comparisons use APR calculated on a $30,000 unsecured loan over 5 years. These are entirely different benchmarks.

For personal loans, the key things to check are:

- APR, which includes interest plus fees and is a better cost measure than the headline rate alone

- Origination fees, which vary widely between lenders

- Prepayment penalties, which can catch you out if you want to pay the loan off early

- Repayment flexibility, since shorter terms mean higher repayments but less total interest

The lowest advertised rate doesn't always mean the best long-term deal, particularly when fees, terms, and features are ignored. This is as true for personal loans as it is for home loans.

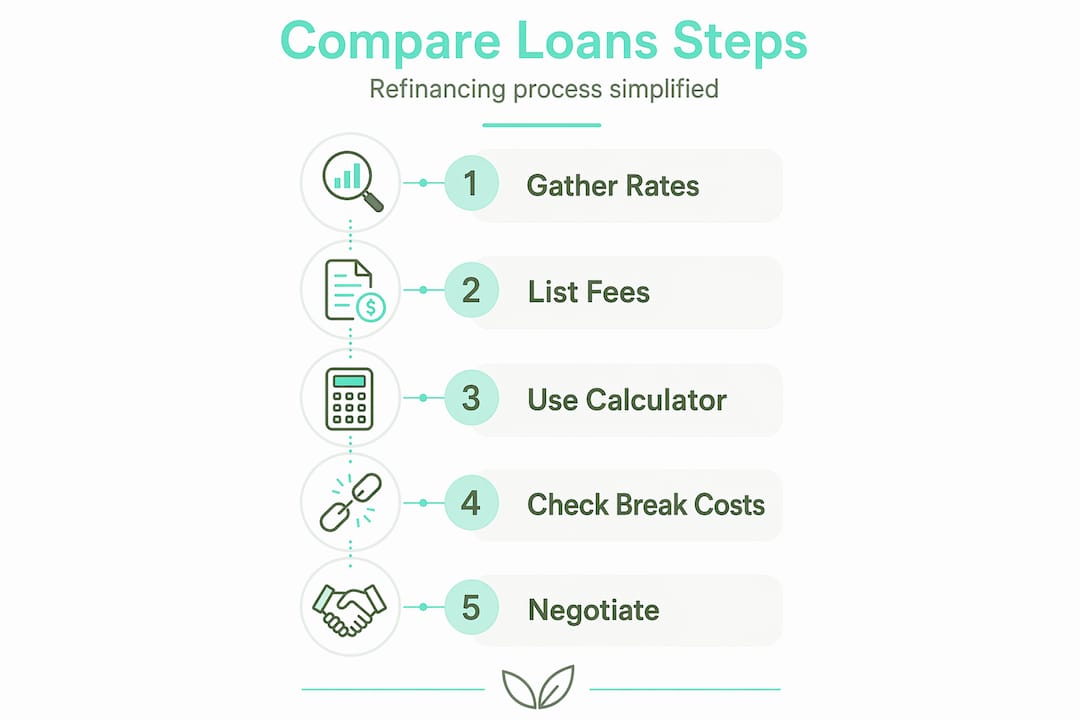

Steps to compare loans when refinancing

Refinancing is where loan comparison skills pay off most directly. But the maths is more involved than a simple rate comparison.

Start by recording your current loan details: your interest rate, remaining term, regular repayments, and any fees attached to the loan. Then get a clear picture of what it will cost to leave.

- Discharge fees typically run between $150 and $500

- Application fees on the new loan range from $0 to $600

- Break costs on fixed loans can run from a few hundred dollars to more than $50,000 depending on how much of the fixed term remains

Once you have those figures, use a refinance calculator to find your break-even point. That's the month at which your ongoing savings from the lower rate exceed the upfront costs of switching. Refinancing savings depend on balancing upfront costs and potential ongoing savings, and that analysis is worth doing carefully.

Don't overlook the option of negotiating with your current lender first. Many lenders will match a competitor's rate to keep your business, which avoids switching costs entirely.

Pro Tip: Always get an exact break cost quote in writing before refinancing a fixed-rate loan. Estimates can be wildly inaccurate, and the real figure can reverse your perceived savings entirely.

My take on what borrowers consistently miss

I've worked with enough borrowers to know that comparison rates get misread constantly. People treat the number as a definitive ranking when it's really just a standardised estimate built on assumptions that may have nothing to do with their situation.

The borrowers who get the best outcomes are the ones who use comparison rates as a filter, not a verdict. They shortlist loans with lower comparison rates, then dig into the actual fees, features, and total costs for their specific loan size and behaviour. An offset account on a $700,000 loan with $50,000 sitting in it will save far more than any comparison rate calculation will show you.

Break costs are the other thing I see catch people off guard. The effective true cost of a loan depends on borrower behaviour, size, term, features, and refinance strategy. Not just the published rate. Treat comparison tools as the starting point they are, then go deeper before you commit.

— Daniel

Compare smarter with Decentloans

Understanding loan comparison is one thing. Having someone do the legwork for you is another.

At Decentloans, we specialise in asset finance and help Australian borrowers find the best loan offers without the headache of doing it alone. We handle your application, compare headline and comparison rates across lenders, and factor in fees, features, and your actual borrowing situation. That means your credit file stays protected while we do the searching. Whether you're purchasing an asset or refinancing an existing debt, we make the process straightforward and transparent. Reach out to the Decentloans team and let us find the right loan for your circumstances.

FAQ

What is a comparison rate in Australia?

A comparison rate combines a loan's interest rate and most mandatory fees into a single annual percentage, calculated on a $150,000 loan over 25 years. It's required by law to be displayed alongside all advertised home loan rates.

Why does the comparison rate differ from the advertised rate?

The advertised rate is the base interest rate only. The comparison rate adds fees like establishment and ongoing service charges, so it gives a more complete picture of the loan's true cost.

Can I compare home loan and personal loan rates directly?

No. Home loan comparison rates use a $150,000/25-year benchmark, while personal loan APR is calculated on a $30,000 unsecured loan over 5 years. The two figures are not directly comparable.

How do I know if refinancing is worth it?

Calculate all switching costs, including discharge fees, application fees, and any break costs on a fixed loan, then use a refinance calculator to find the break-even point where savings exceed those upfront costs.

Do comparison rates include offset account benefits?

No. Offset accounts reduce your effective interest cost but are not factored into comparison rate calculations, which is one reason why the comparison rate alone can be a misleading guide to total loan cost.