Getting knocked back on a loan application, or watching it drag on for weeks, often has less to do with your credit score than with when and how you submitted it. Knowing how to time a loan application correctly is one of the most underrated skills a borrower can develop. This guide walks you through the preparation, strategic timing, execution, and post-submission steps that separate a clean approval from a frustrating delay.

Table of Contents

- Key takeaways

- Preparation steps before you apply

- Timing your loan application submissions correctly

- Executing the application: avoiding common delays

- Verifying and monitoring after submission

- My honest take on loan application timing

- How Decentloans can help you apply with confidence

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Start credit prep early | Review your credit report at least 90 days before applying to catch and fix errors in time. |

| Use the rate shopping window | Submit multiple applications for the same loan type within 14 to 45 days so they count as one inquiry. |

| Apply on weekday mornings | Lenders process faster during business hours, so early weekday submissions get more attention sooner. |

| Complete your packet first | A thorough, accurate document package avoids back-and-forth delays and speeds up underwriting. |

| Monitor after submission | Keep your credit stable and respond quickly to any lender requests during the review period. |

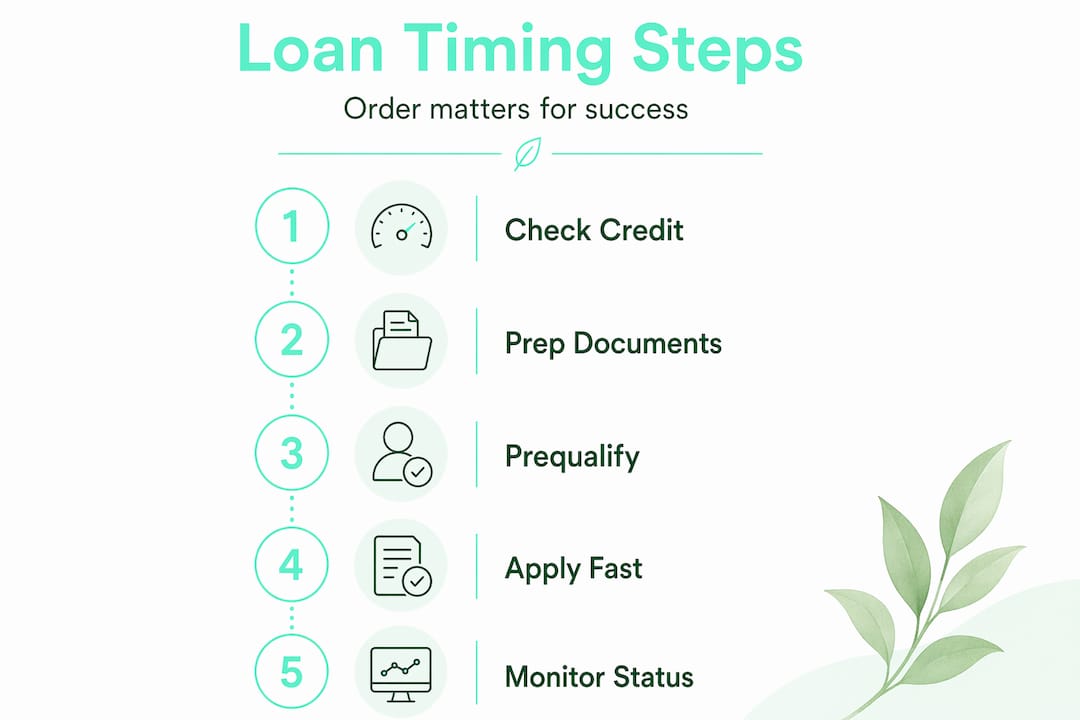

Preparation steps before you apply

The industry term for what most people call "getting ready to apply" is pre-application due diligence, and it is where most borrowers either set themselves up for success or quietly sabotage their chances.

The single most important step is reviewing your credit report well before you need the money. Start at least 90 days prior to audit your credit, identify errors, and give yourself enough time to dispute anything inaccurate. The CFPB also recommends reviewing credit reports early so corrections can be processed before your formal application goes in. Waiting until the week before you apply leaves no room to fix anything.

Beyond credit, you need to understand your debt-to-income ratio (DTI). This is the percentage of your gross monthly income that goes toward debt repayments. Most lenders want to see a DTI below 43%, though lower is always better. Calculate yours before you apply so there are no surprises.

Pro Tip: If your DTI is too high, paying down a small revolving balance before applying can shift the number meaningfully in a short period.

Here is a practical checklist of what to gather before you submit:

- Recent payslips (last two to three months)

- Tax returns or notices of assessment for the past two years

- Bank statements covering at least three months

- Government-issued photo ID

- Details of existing debts, including balances and monthly repayments

- Proof of assets if relevant (property, vehicles, savings)

Familiarise yourself with the specific requirements of the lender you are targeting. Different loan types, whether personal, home, or asset finance, carry different documentation expectations. Arriving prepared means lenders expect identity, credit, and financial evidence in a complete package before underwriting begins.

Timing your loan application submissions correctly

This is where most borrowers leave money, and credit score points, on the table. The concept you need to understand is called the Rate Shopping Rule, and it is built into how credit scoring models work.

FICO's inquiry shopping window consolidates multiple loan inquiries of the same type into a single credit event, provided they occur within a 14 to 45 day window. That means you can apply to five lenders for the same type of loan and take only one hit to your score, as long as you cluster those applications within that window. This is the single most important loan application timing tip most borrowers never hear.

Here is how to apply this in practice:

- Run prequalifications first. Most lenders offer a soft-inquiry prequalification that does not affect your score. Use these to narrow your shortlist before triggering any hard inquiries.

- Fix your target window. Once you are ready to formally apply, choose a 14-day window and submit all formal applications within it.

- Apply on a weekday morning. Fastest processing happens when you apply during normal business hours, avoiding public holidays and late-week submissions that sit unprocessed until Monday.

- Avoid applying after major financial changes. A recent job change, a new credit card, or a large purchase can raise lender flags. Give yourself at least 60 days of financial stability before formally applying.

- Do not apply for unrelated credit in the same period. Each hard inquiry drops your score by roughly 5 to 10 points and stays on your report for two years. Avoid car finance, credit cards, or any other credit product during your loan application window.

| Timing mistake | Likely consequence |

|---|---|

| Applying across multiple weeks | Multiple hard inquiries, unnecessary score damage |

| Submitting on a Friday afternoon | Application sits unprocessed over the weekend |

| Applying right after a job change | Lender flags income instability, may request more documents |

| Skipping prequalification | Hard inquiry wasted on a lender unlikely to approve you |

Pro Tip: Prequalify with three to five lenders, then formally apply to your top two or three within the same two-week window. You get comparison without the credit damage.

Executing the application: avoiding common delays

Knowing when to submit is only half the equation. How you submit determines whether approval takes hours or weeks. Approval can come the same day for personal loans when the application is complete and error-free, with funding following within one to three business days.

The most common execution mistakes are entirely avoidable:

- Typos and incorrect details. A wrong employer name, a transposed digit in your income, or a mismatched address can trigger a resubmission request. Incorrect information causes lenders to ask for corrections, adding days to the process.

- Stale documents. Payslips from six months ago, or a bank statement that is more than 90 days old, are often rejected outright. Lenders pull underwriting based on how recent your supporting documents are.

- Submitting before you are ready. Incomplete packets create document request loops that prolong approval timelines significantly. Correct timing often means waiting until you have everything, not just submitting on a particular day.

- Applying to the wrong lender for your profile. A lender specialising in prime borrowers will not approve a thin credit file. Match your profile to the lender before you apply.

Prequalify before formally applying to gauge your eligibility without triggering a hard inquiry. Only move to a formal application once you have confirmed the loan amount, term, and purpose are finalised.

Verifying and monitoring after submission

Once your application is in, the work is not over. The loan application process timeline from submission to approval varies by loan type. Personal loans can resolve within a day or two. Home loans typically take two to four weeks. Asset finance sits somewhere in between.

During this period, keep a close eye on the following:

- Your inbox and phone. Lenders contact you quickly when they need more information. A 24-hour delay in responding can push your file to the back of the queue.

- Your credit profile. Do not apply for anything else, do not close existing accounts, and avoid large purchases on credit. Lenders sometimes do a second credit check before settlement.

- Your document expiry dates. If the process drags past 90 days, some documents may need refreshing before the lender will proceed.

- Lender communication patterns. If you have not heard anything within the expected window, a polite follow-up call is appropriate. Ask for a status update and whether any additional information is required.

A proactive, organised borrower almost always gets faster outcomes than one who submits and waits passively.

My honest take on loan application timing

I have seen borrowers with excellent credit scores get delayed or declined simply because they applied at the wrong moment or submitted a messy packet. And I have seen borrowers with average credit sail through because they prepared properly and timed everything well.

The misconception I encounter most often is that your credit score is the main lever. It matters, but lenders are also assessing your readiness. A complete, accurate, well-timed application signals that you are an organised borrower who is unlikely to create problems down the track.

What I have found consistently is that patience in the preparation phase pays off more than urgency. Rushing an application to meet an arbitrary deadline almost always creates more problems than it solves. If you are not ready, wait two more weeks and do it properly.

The borrowers who get the best outcomes are the ones who treat the application as a process, not an event.

— Daniel

How Decentloans can help you apply with confidence

Timing and preparation matter, but navigating multiple lenders, document requirements, and credit implications on your own is a lot to manage. That is exactly what Decentloans is built for.

Decentloans is an asset finance broker specialist that handles the legwork for you, from identifying the right lenders for your profile to managing your application so your credit file stays protected. Rather than submitting multiple applications yourself and risking unnecessary hard inquiries, Decentloans coordinates the process to keep your credit impact to a minimum. Whether you are applying for personal finance, a home loan, or asset finance, the team guides you through every step so nothing gets missed and nothing gets delayed. Reach out to Decentloans for personalised support and a smarter path to approval.

FAQ

When is the right time to submit a loan application?

The right time is when your credit report is clean, your documents are current, and you have completed prequalification with your shortlisted lenders. Submitting on a weekday morning within a consolidated application window gives you the best chance of fast processing.

How does the rate shopping window protect my credit score?

FICO consolidates multiple inquiries for the same loan type into a single credit event when they occur within 14 to 45 days, meaning you can compare lenders without taking repeated score hits.

What documents do I need for a loan application?

Most lenders require recent payslips, tax returns, bank statements, photo ID, and details of existing debts. Having these ready before you apply prevents delays caused by document request loops.

How long does loan approval take?

Personal loans can be approved the same day and funded within one to three business days when the application is complete. Home loans typically take two to four weeks depending on the lender and complexity.

Does applying to multiple lenders hurt my credit score?

It can, but only if you spread applications across multiple weeks. Clustering formal applications within a 14-day window means they are treated as a single inquiry under standard credit scoring models.